BREAKING DOWN THE CONCEPT OF NBFCs

While understanding the basic idea of a Non-Banking Financial Companies (NBFCs), we need to know what exactly NBFCs are. As per law, A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act, 1956 engaged in the business of loans and advances, acquisition of shares / stocks / bonds / debentures / securities issued by Government or local authority or other marketable securities of a like nature, leasing, hire-purchase, insurance business, chit business but does not include any institution whose principal business is that of agriculture activity, industrial activity, purchase or sale of any goods (other than securities) or providing any services and sale/purchase/construction of immovable property. In lay man language Non-Banking Financial Companies (NBFCs) are the financial institutions that offer the banking services but does not comply with the legal definition of a bank, i.e. it does not hold a bank license.

SALIENT FEATURES OF NBFCs

- The NBFCs are allowed to accept/renew public deposits for a minimum period of 12 months and maximum period of 60 months. They cannot accept deposits repayable on demand.

- NBFCs cannot offer interest rates higher than the ceiling rate prescribed by RBI from time to time. The present ceiling is 12.5 per cent per annum. The interest may be paid or compounded at rests not shorter than monthly rests.

- NBFCs cannot offer gifts/incentives or any other additional benefit to the depositors.

- NBFCs (except certain AFCs) should have minimum investment grade credit rating.

- The deposits with NBFCs are not insured.

- The repayment of deposits by NBFCs is not guaranteed by RBI.

- There are certain mandatory disclosures about the company in the Application Form issued by the company soliciting deposits.

TYPES OF NBFCs

The common types of NBFCs in India today are:

The Mutual Benefit Finance Companies also called as “Nidhis”, are the non-banking finance companies that enable its members to pool their money with a predetermined investment objective. The main sources of funds are share capital, deposits from its members, deposits from the general public.In other words, any company which has been notified by the Central Government as Nidhis under the section 620A of Companies Act, 1956 work as a mutual benefit finance company. These are one of the oldest forms of non-banking finance companies wherein the owners of the company are also its clients and pool their resources with the intent to secure loans at a low interest rate at the time the funds are required.

IC means any company which is a financial institution carrying on as its principal business the acquisition of securities.

LC means any company which is a financial institution carrying on as its principal business the providing of finance whether by making loans or advances or otherwise for any activity other than its own but does not include an Asset Finance Company.

An AFC is a company which is a financial institution carrying on as its principal business the financing of physical assets supporting productive/economic activity, such as automobiles, tractors, lathe machines, generator sets, earth moving and material handling equipments, moving on own power and general purpose industrial machines. Principal business for this purpose is defined as aggregate of financing real/physical assets supporting economic activity and income arising therefrom is not less than 60% of its total assets and total income respectively.

IFC is a non-banking finance company a) which deploys at least 75 per cent of its total assets in infrastructure loans, b) has a minimum Net Owned Funds of ₹ 300 crore, c) has a minimum credit rating of ‘A ‘or equivalent d) and a CRAR of 15%.

IDF-NBFC is a company registered as NBFC to facilitate the flow of long term debt into infrastructure projects. IDF-NBFC raise resources through issue of Rupee or Dollar denominated bonds of minimum 5 year maturity. Only Infrastructure Finance Companies (IFC) can sponsor IDF-NBFCs.

NBFC-MFI is a non-deposit taking NBFC having not less than 85% of its assets in the nature of qualifying assets which satisfy the following criteria:

- loan disbursed by an NBFC-MFI to a borrower with a rural household annual income not exceeding ₹ 1,00,000 or urban and semi-urban household income not exceeding ₹ 1,60,000;

- loan amount does not exceed ₹ 50,000 in the first cycle and ₹ 1,00,000 in subsequent cycles;

- total indebtedness of the borrower does not exceed ₹ 1,00,000;

- tenure of the loan not to be less than 24 months for loan amount in excess of ₹ 15,000 with prepayment without penalty;

- loan to be extended without collateral;

- aggregate amount of loans, given for income generation, is not less than 50 per cent of the total loans given by the MFIs;

- loan is repayable on weekly, fortnightly or monthly instalments at the choice of the borrower

CIC-ND-SI is an NBFC carrying on the business of acquisition of shares and securities which satisfies the following conditions:-

- it holds not less than 90% of its Total Assets in the form of investment in equity shares, preference shares, debt or loans in group companies;

- its investments in the equity shares (including instruments compulsorily convertible into equity shares within a period not exceeding 10 years from the date of issue) in group companies constitutes not less than 60% of its Total Assets;

- it does not trade in its investments in shares, debt or loans in group companies except through block sale for the purpose of dilution or disinvestment;

- (d) it does not carry on any other financial activity referred to in Section 45I(c) and 45I(f) of the RBI act, 1934 except investment in bank deposits, money market instruments, government securities, loans to and investments in debt issuances of group companies or guarantees issued on behalf of group companies.

- (e) Its asset size is ₹ 100 crore or above and

- (f) It accepts public funds

NBFC-Factor is a non-deposit taking NBFC engaged in the principal business of factoring. The financial assets in the factoring business should constitute at least 50 percent of its total assets and its income derived from factoring business should not be less than 50 percent of its gross income.

It is a form of non-banking financial company which is engaged in the principal business of financing of acquisition or construction of houses that includes the development of plots of lands for the construction of new houses.

The Chit Fund Company is a financial institution engaged in the principal business of managing, conducting and supervising the chit scheme. The Chit Fund Company collects the subscriptions by way of installments over a definite period from the certain number of subscribers and distributes the same as a prize amongst them. The operations of the Chit Fund Company are governed by the Chit Fund Act, 1982, administered by the State Governments. While the deposit taking activities of, such firm is regulated by the Reserve Bank of India.

EL means any company which is a financial institution carrying on as its principal business, the activity of leasing of equipment.

HP means any company which is a financial institution carrying on as its principal business the activity of hire purchase transactions

It is yet another form of a financial institution engaged in the principal business of accepting deposits, under any scheme or arrangement or in any other form and not being asset financing, investment, Loan Company.Simply, the Residuary Non-Banking Company primarily deal in accepting deposits in any form and investing these in the approved securities. The operations of such company are regulated by RBI and in addition, to the liquid assets, it maintains its investments as per the RBI directions.

REGISTRATION REQUIREMENTS

As per Section 45-IA of the RBI Act, 1934, no company can commence or carry on business of a non-banking financial institution without obtaining a certificate of registration. The requirement for registration as a NBFC are:

- It should be a company registered under Section 3 of the companies Act, 1956

- It should have a minimum net owned fund of ₹ 200 lakh.

Net owned funds is the balance of “owned funds” minus the amount of investment in shares of subsidiaries, companies in the same group and all other NBFCs, book value of debentures, bonds, outstanding loans and advances including hire purchase and lease finance made to and deposits with subsidiaries and companies in the same group. Owned funds is the aggregate of paid-up equity capital , preference shares which are compulsorily convertible into equity, free reserves , balance in share premium account and capital reserves representing surplus arising out of sale proceeds of asset, excluding reserves created by revaluation of asset, after deducting therefrom accumulated balance of loss, deferred revenue expenditure and other intangible assets.

LIST OF DOCUMENTS

Documents required for

registration as Type I – NBFC-ND

An indicative list of basic documents/information to be furnished along with the application form:

| Sr. No. | Requirements to be complied with and documents to be submitted to RBI by Companies for obtaining certificate and Registration from RBI as NBFC |

|---|---|

| 1 | Certified copies of Certificate of Incorporation and Certificate of Commencement of Business in case of public limited companies. |

| 2 | Certified copies of extract of only the main object clause in the MOA relating to the financial business. |

| 3 | Board resolution stating that: a) the company is not carrying on any NBFC activity/stopped NBFC activity and will not carry on/commence the same before getting registration from RBI b) the UIBs in the group where the director holds substantial interest or otherwise has not accepted any public deposit in the past /does not hold any public deposit as on the date and will not accept the same in future c) the company has formulated “Fair Practices Code” as per RBI Guidelines d) the company has not accepted public funds in the past/does not hold any public fund as on the date and will not accept the same in the future without the approval of Reserve Bank of India e) the company does not have any customer interface as on date and will not have any customer interface in the future without the approval of Reserve Bank of India |

| 4 | Copy of Fixed Deposit receipt & bankers certificate of no lien indicating balances in support of NOF |

| 5 | For companies already in existence, the Audited balance sheet and Profit & Loss account along with directors & auditors report or for the entire period the company is in existence, or for last three years , whichever is less, should be submitted |

| 6 | Banker’s report in respect of applicant company, its group/subsidiary/associate/holding company/related parties, directors of the applicant company having substantial interest in other companies The Banker’s report should be about the dealings of these entities with these bankers as a depositing entity or a borrowing entity. Note: Please provide bankers report from all the bankers of each of these entities and provide the report for all the entities. The details of deposits and loans balances as on the date of application and the conduct of the account should be specified. |

Documents required for registration as Type II – NBFC-ND (including new applications of NBFC-MFI, NBFC-Factor, NBFC-IDF)

An indicative list of basic documents/information to be furnished along with the application form:

| Sr. No. | Requirements to be complied with and documents to be submitted to RBI by Companies for obtaining certificate and Registration from RBI as NBFC |

|---|---|

| 1 | Certified copies of Certificate of Incorporation and Certificate of Commencement of Business in case of public limited companies. |

| 2 | Certified copies of extract of only the main object clause in the MOA relating to the financial business. |

| 3 | Board resolution stating that: (a) the company is not carrying on any NBFC activity/stopped NBFC activity and will not carry on/commence the same before getting registration from RBI. (b) the company has not accepted any public deposit, in the past (specify period)/does not hold any public deposit as on the date and will not accept the same in future without the prior approval of Reserve Bank of India. (c) the UIBs in the group where the director holds substantial interest or otherwise has not accepted any public deposit in the past does not hold any public deposit as on the date and will not accept the same in future. (d)the company has formulated “Fair Practices Code” as per RBI Guidelines. |

| 4 | Copy of Fixed Deposit receipt & bankers certificate of no lien indicating balances in support of NOF |

| 5 | For companies already in existence, the Audited balance sheet and Profit & Loss account along with directors & auditors report or for the entire period the company is in existence, or for last three years, whichever is less, should be submitted |

| 6 | Copy of the certificate of highest educational and professional qualification in respect of all the directors |

| 7 | Copy of experience certificate, if any, in the Financial Services Sector (including Banking Sector) in respect of all the directors |

| 8 | Banker’s report in respect of applicant company, its group/subsidiary/associate/holding company/related parties, directors of the applicant company having substantial interest in other companies The Banker’s report should be about the dealings of these entities with these bankers as a depositing entity or a borrowing entity. Note: Please provide bankers report from all the bankers of each of these entities and provide the report for all the entities. The details of deposits and loans balances as on the date of application and the conduct of the account should be specified. |

In addition to the Documents required for registration as Type II – NBFC-ND, following list of documents/information to be submitted by the NBFC-MFI applicant:

- Board resolution stating that:

(a) the company will be a member of all the Credit Information Companies and will be a member of at least one Self Regulatory Organisation

(b) the company will adhere to the regulations regarding pricing of credit, Fair Practices in lending and non-coercive method of recovery as per RBI Guidelines

(c) the company has fixed internal exposure limits to avoid any undesirable concentration in specific geographical locations

(d) the company is not licensed under Section 25 of the Companies Act, 1956 / Section 8 of the Companies Act, 2013. - Roadmap for achieving 85% qualifying assets.

In addition to the Documents required for registration as Type II – NBFC-ND, following list of documents / information to be submitted by the NBFC-Factor applicant:

- Board Resolution enclosing roadmap that the company will have financial assets in the factoring business constituting at least 50% of its total assets and its income derived from factoring business will not less than 50% of its gross income (Specify the time frame)

In addition to the Documents required for registration as Type II – NBFC-ND, following list of documents / information to be submitted by the NBFC-IDF applicant:

- No objection Certificate from RBI issued to NBFC-IFC for sponsoring the NBFC-IDF.

- Copy of Tripartite Agreement between the concessionaire, the Project Authority and NBFC-IDF.

- Details of change in the management of the sponsor company during last financial year till date, if any, and reasons thereof.

- Source of startup capital of the company with documentary evidence. NBFC-IDF would raise resources through issue of either Rupee or Dollar denominated Bonds of minimum 5-year maturity.

FORMATION PROCEDURE

- A company with main object clause/ ancillary clause for carrying out NBFI activities (check object clause)

- Obtain checklist of requirements from RBI website

- Fill up prescribed form, available on RBI website, according to instructions with the requirements

- Fill up the e‐form provid de in excel format

- Get the required certifications of the statutory auditors/chartered auditors/chartered accountants accountants (as the case may be)

- Submit softcopy on RBI website before submission of the hard copy.

COMMENCEMENT OF BUSINESS

- NBFC must commence commence its business business within 6 months from the date of CoR

- If not commenced commenced within 6 months , CoR will stand withdrawn

- No c hange in control prior to commencement of its business

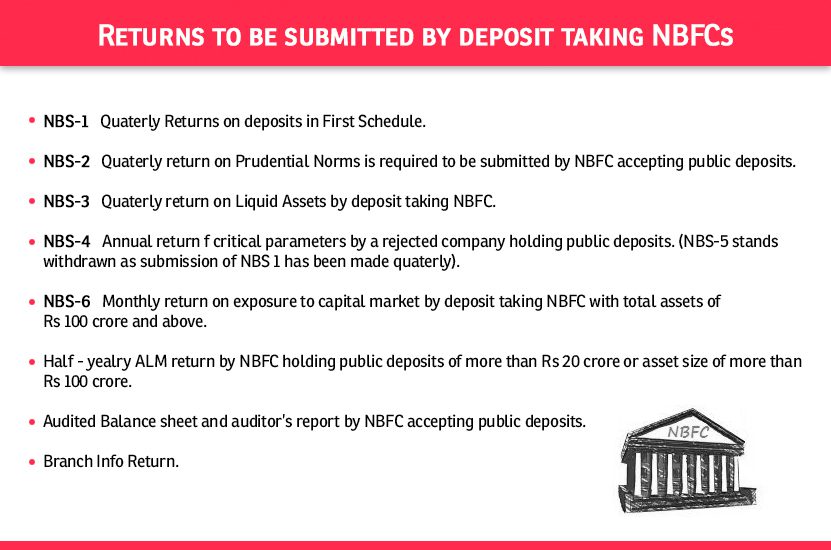

RETURNS

Returns to be submitted by deposit taking NBFCs

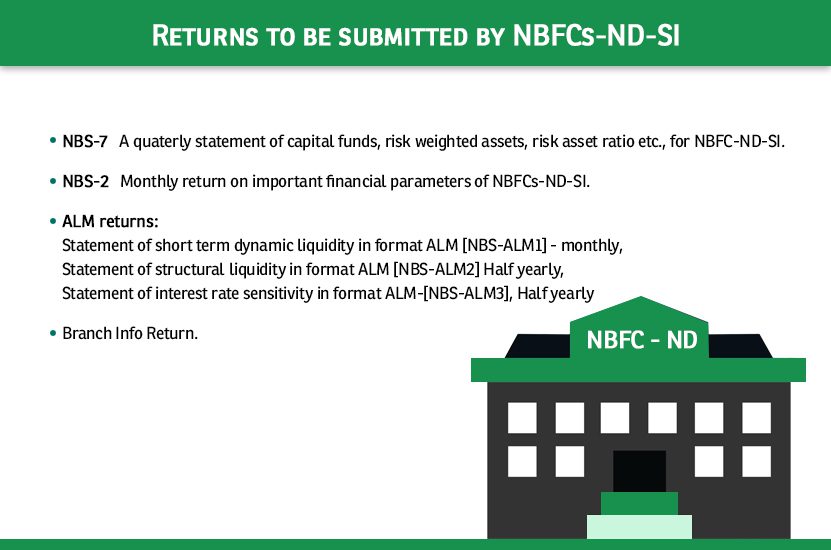

Returns to be submitted by NBFCs-ND-SI

Quarterly return on important financial parameters of non deposit taking NBFCs having assets of more than ₹ 50 crore and above but less than ₹ 100 crore

- Basic information like name of the company, address, NOF, profit / loss during the last three years has to be submitted quarterly by non-deposit taking NBFCs with asset size between ₹ 50 crore and ₹ 100 crore.

COMPLIANCES

- COMPLIANCE CHECKLIST FOR NON-DEPOSIT TAKING NBFC WITH RBI

Annual compliances

| S No. | Particulars | Time limit |

|---|---|---|

| 1 | Unaudited March Monthly return/NBS7 | on or before 30th June |

| 2 | Audited March Monthly return/NBS7 | Upon completion |

| 3 | Statutory Auditors certificate on Income & Assets | on or before 30th June |

| 4 | Information about Cos having FDI/Foreign Funds | on or before 30th June |

| 5 | Resolution of Non-acceptance of Public Deposit | before commencement of new Financial year |

| 6 | File Audited Annual Balance Sheet and P&L Account | One month from the date of signoff |

| 7 | Declaration of Auditors to Act as Auditors of the Company | annual basis |

Monthly compliances

| S No. | Particulars | Time limit |

|---|---|---|

| 1 | Monthly Return | by 7th of every month |

| 2 | Upload monthly return on www.dnbsinfinet.org (OLD) | by 7th of every month |

Periodical compliances

| S No. | Particulars | Time limit |

|---|---|---|

| 1 | Appoinment of Director(Annexure-III) | within 30 days of appointment |

| 2 | Upload monthly return on www.dnbsinfinet.org (OLD) | within 30 days of resignation |

| 3 | Resignation of Director(Form- 32 + Challan Receipt) |

COMPLIANCE CHECKLIST FOR NON DEPOSIT TAKING NBFC WITH NSC

3. Letter from Directors for filing UIM

| S No. | Particulars | Time limit |

|---|---|---|

| 1 | Filing of Listing Agreement of Issued Series | Within 30 days of Issuance |

| 2 | Publishing of Unaudited Half-yearly Result in two newspaper | Within 30 days from the end of Half-year |

| 3 | File Half-yearly Audited Result with NSE via mail | Within 30 days from the end of Half-year |

| 4 | File Quaterly result (Balance Sheet and P&L) via mail | Within 90 days from the end of Quarter |

| 5 | Filing Umbrella Information Memorandum/Shelf Offer Document + below letters: | At the end of Financial Year |

| 1. Letter from CRISIL for filing UIM | ||

| 2. Letter from AXIS Bank (Debenture Trustee) for filing UIM | ||

| 4. Certifed true copy of the resolution authorizing filing of UIM | ||

| 5. Certifed true copy of the blanket resolution covering Debt issuances for filing UIM | ||

| 6. Certify compliance as per Chapter VI of SEBI (DIP) Guidelines 2000 & Sch-II of Companies Act,1956 | ||

| 7. Obtain In-principle approval letter from NSE post filing |

COMPLIANCE CALENDAR

| Sr No | Name of the Return | Short Name | Periodicity | Reference Date | Reporting Time | Due on | Purpose | To be submitted by |

|---|---|---|---|---|---|---|---|---|

| 1 | Quarterly Returns By deposit taking NBFCs (As required by “Non-Banking Financial Companies Acceptance of Public Deposits (Reserve Bank) Directions, 1998”.) |

NBS1 | Quarterly | 31st March/ 30th June/ 30th Sept/ 31st Dec | 15 days | 15th April/ 15th July/ 15th Oct/ 15th Jan |

Details of Assets And Liabilities | NBFCs-D |

| 2 | Quarterly Statement of Capital Funds, Risk Assets etc as required under the Non-Banking Financial Companies Prudential Norms (Reserve Bank) Directions 2007 By deposit taking NBFCs | NBS2 | Quarterly | 31st March/ 30th June/ 30th Sept/ 31st Dec | 15 days | 15th April/ 15th July/ 15th Oct/ 15th Jan |

Capital Funds, Risk Assets, Asset Classification etc | NBFCs-D |

| 3 | Quarterly Return on Statutory Liquid Assets as per Section 45 IB of the Act By Deposit Taking NBFCs | NBS3 | Quarterly | 31st March/ 30th June/ 30th Sept/ 31st Dec | 15 days | 15th April/ 15th July/ 15th Oct/ 15th Jan |

Statutory Liquid Assets | NBFCs-D |

| 4 | Annual Return on Repayment of Deposits by the Rejected Companies holding Public Deposits (The return was subsequently simplified for better response) | NBS4 | Annual | March 31 | 30 days | May 01 | Details of Public Deposits, Other Liabilities | NBFCs holding public deposits whose application for Certificate of Registration under Section 45-IA of RBI Act, 1934 have been rejected |

| 5 | Monthly Return on Capital Market Exposure | NBS6 | Monthly | As at the end of the month | 7 days | 7th day of next month | Details of Capital Market Exposure | NBFCs-D |

| 6 | Quarterly Return of Capital Funds, Risk-Asset Ratio from NBFCs-ND-SI (Supervisory Return) | NBS7 | Quarterly | 31st March/ 30th June/ 30th Sept/ 31st Dec | 15 days | 15th April/ 15th July/ 15th Oct/ 15th Jan |

Capital Funds, Risk Assets, Risk Weighted off-balance sheet items (Non-Funded Exposures), Asset Classification etc. | NBFCs-ND-SI |

| 7 | Asset-Liability Management (ALM) Return | ALM | Half yearly | 31st March/ 30th Sept | 1 month | 30th April/ 30th Oct | Structural Liquidity, Short-term dynamic liquidity, Interest Rate sensitivity etc. | NBFCs-D having public deposit of Rs 20 crore and/or asset size of more than Rs. 100 crore |

| 8 | A Statement of short term dynamic liquidity in format ALM -NBS-ALM1 | ALM-1 | Monthly | As at end of the month | 10 days | 10th day of next month | Short-term dynamic liquidity | NBFC-ND-SI |

| 9 | Statement of structural liquidity in format ALM – NBS-ALM2 | ALM-2 | Half yearly | 31st March/ 30th Sept | 20 days | 20th April/ 20th Oct | Structural liquidity | NBFC-ND-SI |

| 10 | Statement of Interest Rate Sensitivity in format ALM-NBS-ALM3. | ALM-3 | Half yearly | 31st March/ 30th Sept | 20 days | 20th April/ 20th Oct | Interest Rate sensitivity | NBFC-ND-SI |

| 11 | Monthly Return on Important Financial Parameters of NBFCs not accepting/holding public deposits and having asset size of Rs.100 crore and above | 100 Crore NBFCs-ND-SI |

Monthly | end of every month | 7days | 7th of next month | Sources and Application of Funds, Profit and Loss Account, Asset Classification, Bank’s/FIs exposure on the company, Details of Capital Market Exposure, Foreign Sources etc. | NBFC-ND-SI |

| 12 | Quarterly return to be submitted by non-deposit taking NBFCs with asset size of Rs 50 crore and above but less than Rs 100 crore, | Quarterly. | 31st March/ 30th June/ 30th Sept/31st Dec | within a period of one month from the close of the quarter | Basic information like name of the company, address. NOF, profit / loss during the last three years | |||

| 13 | Quarterly Return to be submitted by NBFCs having overseas investment | Quarterly. | 31st March/ 30th June/ 30th Sept/ 31st Dec | within a period of one month from the close of the quarter | Name of the WOS/JV, Country and date of incorporation Date of NoC from DNBS, Business undertaken |

All NBFCs |

Note: NBFCs-D -> Deposit taking Non-Banking Financial Companies (NBFCs);

NBFCs-ND -> Non-Deposit taking NBFCs.

NBFCs-ND-SI -> Non-Banking Financial Companies (NBFCs) not accepting/holding public deposits and having asset sizes of Rs.100 crore and above (also termed as Systemically Important NBFCs or in short NBFCs-ND-SI)

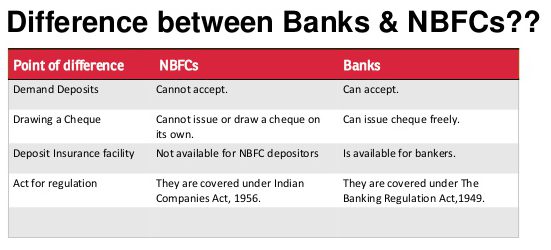

DIFFERENCE BETWEEN BANKS AND NBFCS

An NBFC lends and makes investments, this makes them similar to banks but the differences they have are listed below:

- NBFCs don’t accept Demand Deposits.

- They are not a part of the payment and settlement system and they can’t issue cheques on themselves.

- Deposit Insurance Facility is not available through NBFCs.

POWERS OF RBI WITH REGARD TO NBFCs

RBI does not regulate all financial companies. Housing Finance Companies, Merchant Banking Companies, Stock Exchanges, Companies engaged in the business of stock-broking/sub-broking, Venture Capital Fund Companies, Nidhi Companies, Insurance companies and Chit Fund Companies are NBFCs but they have been exempted from the requirement of registration under Section 45-IA of the RBI Act, 1934 subject to certain conditions.

Other regulators apart from RBI are:

- Chit Funds – Respective State Governments

- Stock broking companies – SEBI

- Insurance companies – IRDA

- Nidhi Companies – Ministry of corporate affairs, Government of India

- Merchant Banking companies – SEBI

- Housing Finance Companies – NHB

- Venture Capital Fund – SEBI

DEPOSITS IN NBFC

- The maximum rate of interest that an NBFC can offer its customers is 12.5%. This interest can be paid or compounded at rests not shorter than a month.

- NBFCs which are allowed to renew/accept public deposits for a minimum time period of 12 months and the maximum time period of 60 months.

- They cannot accept deposits repayable on demand.

- Deposits are not insured.

- Repayment of Deposits is not guaranteed by RBI.

- Obtain the printout of successful submission of the softcopy. Mention the date of submission on the print if date is not appearing on print.

- Submit the hardcopy application in duplicate to regional office of RBI

- Each page in the application file should be numbered

- Prepare the application in triplicate so that a replica is with the applicant for future reference.

KEY POINTS TO REMEMBER WHILE DEPOSITING WITH NBFCs

While making deposits with a NBFC, the following aspects should be borne in mind:

- Public deposits are unsecured.

- A proper deposit receipt which should, besides the name of the depositor/s state the date of deposit, the amount in words and figures, rate of interest payable and the date of maturity should be insisted. The receipt shall be duly signed by an officer authorized by the company in that behalf.

- The Reserve Bank of India does not accept any responsibility or guarantee about the present position as to the financial soundness of the company or for the correctness of any of the statements or representations made or opinions expressed by the company and for repayment of deposits/discharge of the liabilities by the company.

Recent Posts

Recent Comments

Categories

- Acquisitions (1)

- Capital Markets & Listings (5)

- Compliance & Litigation (8)

- condonation of delay scheme (3)

- Consulting (47)

- Corporate Laws (17)

- Corporate World (21)

- Cyber Law (4)

- Debt Collection Company (1)

- Debt Recovery Firm (23)

- Employee Stock Ownership Plan (32)

- Financial (36)

- FSSAI (13)

- Governments (13)

- ICC (2)

- IEPF (1)

- Incorporation (6)

- insolvency and bankruptcy (2)

- Insolvency Education Series (35)

- Insolvency Resolution Process (11)

- internal complaints committee (3)

- Investment Policy (1)

- Liquidation (2)

- Mergers & Acquisitions (6)

- Micro Financing (13)

- Ministry of Corporate Affairs (3)

- MSME (3)

- NBFC (32)

- NBFC Incorporation (6)

- NBFC Registration (7)

- NBFC Weekly Digest (29)

- NGO (6)

- Others (48)

- Peer to Peer Lending (5)

- Phantom Stocks (5)

- PoSH (39)

- Recovery of Bad Debt (12)

- Recovery of Shares (89)

- Removal of Director (15)

- Removal of Disqualification of Directors (32)

- SEBI (7)

- SME IPO (13)

- strike off of companies (9)

- Taxes (5)

- Trademark (7)

- unclaimed shares (27)

- Venture Capital (3)

- Voluntary Liquidation (3)

Tags

Archives

- April 2024 (11)

- March 2024 (9)

- February 2024 (13)

- January 2024 (12)

- December 2023 (17)

- November 2023 (8)

- October 2023 (16)

- September 2023 (12)

- August 2023 (8)

- July 2023 (7)

- June 2023 (8)

- May 2023 (1)

- April 2023 (2)

- March 2023 (11)

- February 2023 (11)

- January 2023 (10)

- December 2022 (12)

- November 2022 (4)

- October 2022 (3)

- September 2022 (3)

- August 2022 (5)

- July 2022 (12)

- June 2022 (12)

- May 2022 (4)

- April 2022 (11)

- March 2022 (19)

- February 2022 (15)

- January 2022 (2)

- November 2021 (2)

- October 2021 (12)

- September 2021 (28)

- August 2021 (14)

- July 2021 (5)

- June 2021 (11)

- May 2021 (8)

- April 2021 (7)

- March 2021 (3)

- February 2021 (7)

- January 2021 (10)

- December 2020 (6)

- November 2020 (13)

- October 2020 (16)

- September 2020 (5)

- August 2020 (3)

- July 2020 (9)

- June 2020 (2)

- May 2020 (1)

- April 2020 (3)

- March 2020 (3)

- February 2020 (4)

- January 2020 (3)

- October 2019 (1)

- August 2019 (10)

- July 2019 (29)

- June 2019 (9)

- May 2019 (11)

- April 2019 (12)

- March 2019 (13)

- February 2019 (8)

- January 2019 (4)

- December 2018 (5)

- October 2018 (7)

- September 2018 (3)

- August 2018 (2)

- July 2018 (8)

- June 2018 (10)

- May 2018 (5)

- April 2018 (6)

- March 2018 (5)

- February 2018 (2)

- January 2018 (6)

- December 2017 (1)

- November 2017 (5)

- October 2017 (5)

- September 2017 (7)

- August 2017 (4)

- July 2017 (1)

Gallery